As an incentive pathway to reduce greenhouse gas (GHG) emissions, carbon credit discussions are becoming increasingly popular. However, not all carbon credits are created equal.

Some credits are designed to help facilities comply with emissions regulations. Others support transportation fuel decarbonization, or finance voluntary climate commitments and durable carbon removals.

Understanding the differences matters because each credit market has different objectives, participants, rules, environmental outcomes, and economic drivers. For project developers, identifying which markets a project may participate in can influence project economics and investment decisions.

Canada’s Carbon Credit Landscape

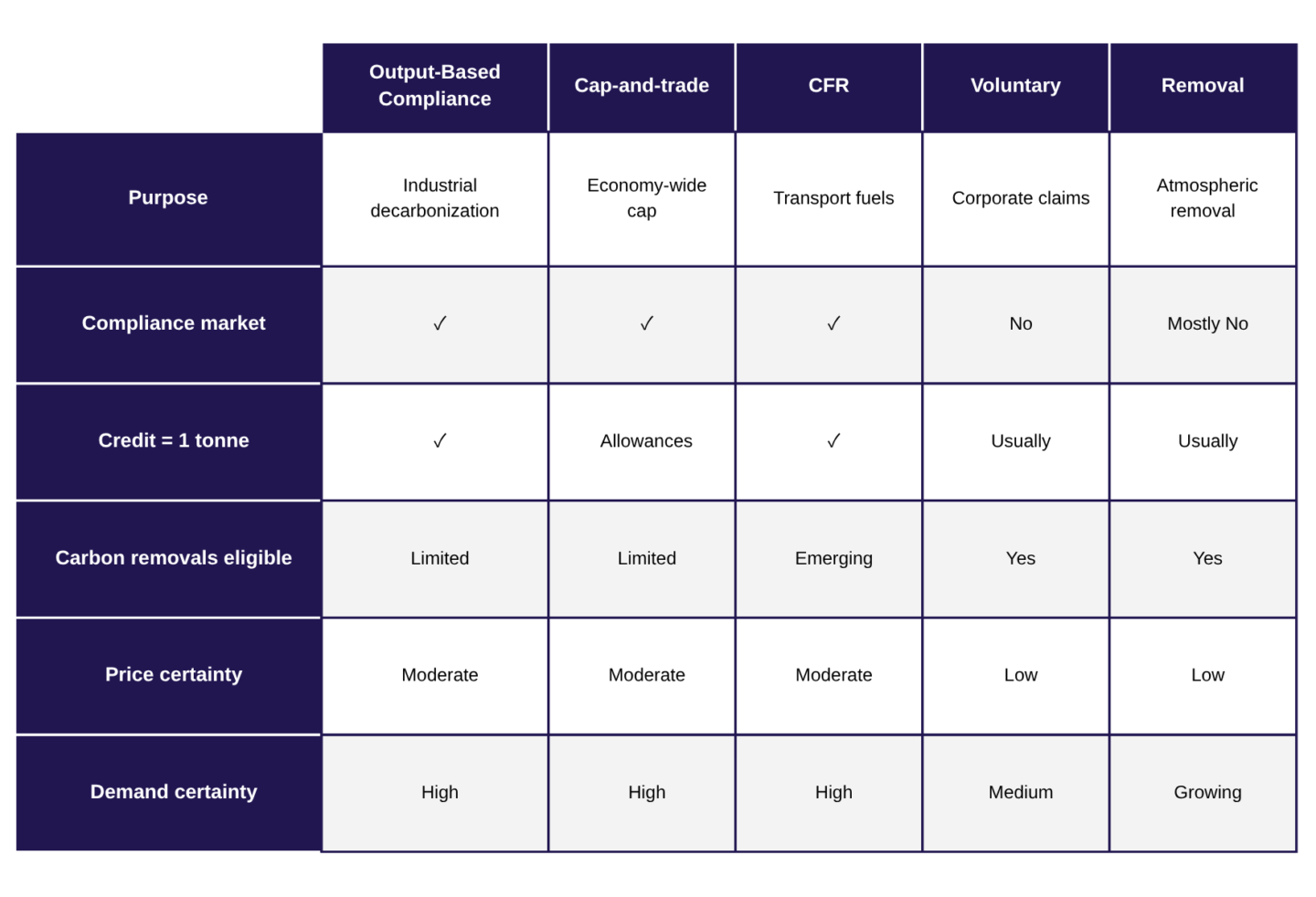

Canada’s carbon markets can broadly be grouped into five categories:

- Output-Based Compliance Systems

- Cap-and-Trade Systems

- Clean Fuel Regulations

- Voluntary Carbon Markets

- Carbon Removal Markets

These markets are not mutually exclusive. Some projects may participate in more than one market, while others may evolve as policies change.

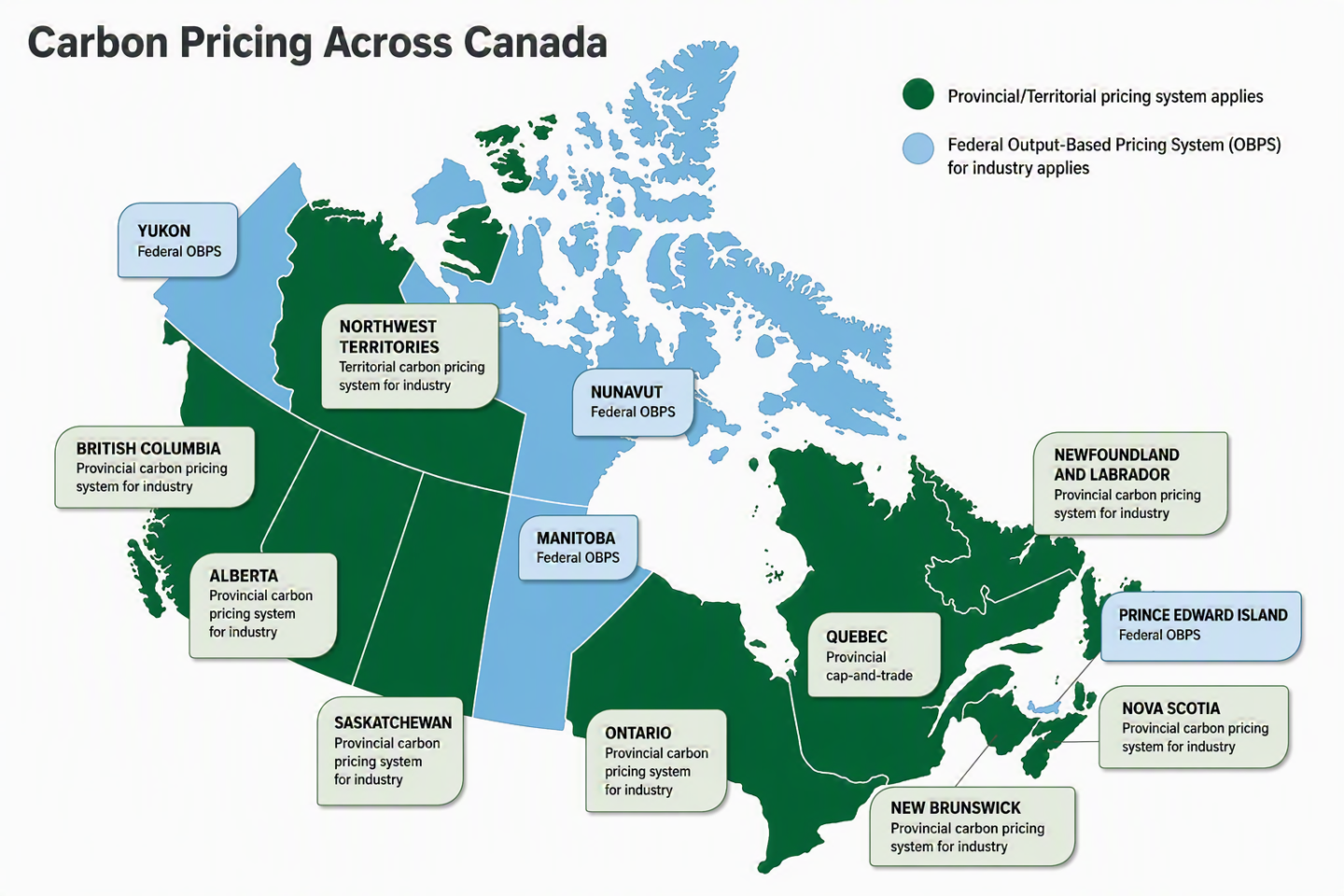

Output-Based Compliance Systems

These systems are designed to reduce emissions from industrial facilities while maintaining competitiveness and minimizing carbon leakage. Provinces and territories are permitted to design their own systems, which are reviewed by the federal government to ensure they meet the national stringency standards. If a province or territory doesn’t design their own system or their system doesn’t meet the federal standards, the federal output-based pricing system (OBPS) applies. Currently four provinces and territories use the federal OBPS, while others have developed and implemented their own carbon pricing systems.

Examples of Canadian pricing systems are:

- Federal OBPS

- British Columbia’s OBPS

- Alberta’s TIER Regulations

- Saskatchewan’s OBPS

- Ontario’s Emissions Performance Standards program

- Quebec’s Cap-and-Trade System

- New Brunswick’s OBPS

- Nova Scotia’s OBPS

- Newfoundland and Labrador’s Carbon Pricing System for Large Industry

These systems establish emissions intensity benchmarks for industrial facilities, and facilities can meet their compliance obligations in multiple ways:

- Reducing their on-site emissions to meet the benchmark (performance credits are generated if the emissions are lower than the benchmark)

- Generating offset credits by investing in emission reductions outside of the regulated facility (e.g. afforestation, mine reclamation, etc.)

- Acquiring compliance credits from other industrial facilities or sequestration companies, or paying directly into the pricing system.

Using an approved protocol, all reductions are quantified before the credits are generated. Facilities can create performance credits in many ways, such as carbon capture, electrification, switching fuels, improving energy efficiency and reducing methane emissions.

Output-based compliance systems can promote market activity and encourage investment in emissions reduction projects because they provide flexibility in how obligations are met. However, project economics can be highly sensitive to benchmark design, policy certainty and confidence in the long-term value of compliance credits. These systems were designed to support reductions rather than removals. Some systems have developed pathways for removal projects to generate credits. For example, Alberta’s Technology Innovation and Emissions Reduction (TIER) regulations now include a protocol for direct air capture with sequestration, which allows eligible projects to generate offset credits.

Cap-and-Trade Systems

Quebec’s approach was to establish an emissions cap that meets federal stringency requirements. Unlike the output-based systems where emissions fluctuate with production levels and available compliance options, a cap-and-trade system enforces a hard emissions limit, and in this case has a declining capacity over time. Quebec’s Cap-and-Trade System is linked to California’s Cap-and-Invest Program through the Western Climate Initiative, creating a larger, integrated carbon market.

To achieve the province’s reduction target, Quebec sets annual emissions caps. At the end of each compliance period, each participating emitter must have allowance credits (one credit is equal to one metric tonne of CO2 equivalent) equal to their period’s total declared and verified emissions. The system covers facilities exceeding specific CO2 thresholds, fuel distributors, or emitters that voluntarily register. Emitters may receive a portion of their allowances through free allocation mechanisms and may also purchase allowances through government auctions or secondary markets. These are three types of emission allowances:

- Emissions units distributed, auctioned or sold by the government’s mutual agreements.

- Offset credits from emission reductions in sectors not subject to the cap-and-trade system.

- Early reductions credits which recognize emissions reductions achieved before the cap-and-trade system started and allowed early acting participants to receive credits.

Each participant in the system must hold an account in the emissions allowance tracking system, where their emission allowances are deposited. All proceeds are paid into the Electrification and Climate Change Fund and finance emission reductions actions.

Just like in the Output-Based Compliance Systems, participants can reduce compliance costs through carbon capture, electrification, switching fuels, improving energy efficiency and reducing methane emissions.

Benefits of a cap-and-trade system include certainty that covered emissions decline over time, incentives to pursue the lowest-cost reductions first, and access to a liquid market under the Western Climate Initiative. However, allowance price volatility (current and future) and variability in investment signals can create challenges. Additionally, Quebec is the only province using a cap-and-trade system, which creates complexities for project developers and market participants navigating multiple carbon pricing and credit systems across Canada.

Clean Fuel Regulations

The Clean Fuel Regulations (CFR) are an important part of Canada’s plan to reduce emissions, as the transportation sector was nearly a quarter of Canada’s total emissions in 2020. The goal of the regulations is to reduce the carbon intensity of transportation fuels over time. The CFR looks at the emissions across the entire lifecycle of fuel, from extraction through processing, distribution and end-use rather than focusing on emissions from only facilities.

Gasoline and diesel suppliers are required to gradually reduce their carbon intensity. They have multiple actions to achieve this separated into categories. Category 1 includes capturing CO2 at a refinery, using CO2 for enhanced oil recovery, using direct air capture to produce synthetic fuels, integrating low-carbon electricity to replace higher-emission electricity, and co-processing conventional crude oil with renewable feedstocks like canola, used cooking oil or soybean oil. Category 2 compliance actions include replacing some fossil fuel with low-carbon fuel like ethanol, renewable diesel, biodiesel or renewable natural gas. Category 3 actions don’t apply to the suppliers as they target replacing fossil fuel vehicles with alternative fuel vehicles, like electric vehicles.

CFR uses a credit market to drive cost-effective emissions reduction solutions. Gasoline and diesel suppliers must create or buy credits to comply with the reduction requirements. Additional credits generated can be sold or kept for use in later years. Credits are generated through the three categories of compliance actions, and each credit represents one tonne of CO2 equivalent reduced.

The CFR is technology neutral, sends a strong signal to decarbonize the transportation infrastructure, and encourages innovative solutions. However, it requires balancing the Canadian competitiveness across the supply chain and maintaining the integrity of credits.

Voluntary Carbon Markets

Voluntary carbon markets provide organizations, businesses, and even individuals with the options to purchase carbon credits which support their climate commitments beyond what they may be obligated to do under regulations. Unlike the three compliance markets above, participation in voluntary markets is not driven by legislation or obligations. Organizations may purchase credits to meet their climate ambitions, address residual emissions, respond to investor expectations, or demonstrate environmental leadership.

Voluntary credits are generated from projects that reduce, avoid or remove greenhouse gas emissions beyond normal operations. These projects are quantified with approved methodologies developed by independent standard bodies and are verified by third-party auditors before credits are issued. Crediting programs include Verra, American Carbon Registry, and Canada’s Greenhouse Gas Offset Credit system.

Voluntary credits can be generated by many activities like afforestation and reforestation projects, improved forest management practices, soil carbon sequestration, biochar production, direct air capture with sequestration, and bioenergy with carbon capture and storage.

Voluntary markets have traditionally supported emission reductions, avoidance and nature-based projects. In Canada the relatively mature compliance markets mean that many emission reductions have a compliance value and as a result, demand may shift toward durable carbon removals or other activities which don’t have a clear compliance value.

Carbon Removal Markets

Carbon removal markets are emerging as a distinct segment of the broader carbon market. Removal markets focus on removing CO2 from the atmosphere and storing it durably unlike the traditional markets, which have focused on avoiding or reducing emissions.

Examples of removals are direct air capture with storage, bioenergy and carbon capture and storage, enhanced rock weathering/mineralization, water-based removal pathways and afforestation/reforestation projects.

Aligned with voluntary carbon markets, the removal market is primarily driven by voluntary demand by organizations that are offsetting residual emissions. Microsoft has purchased most of the removal market credits today, but Frontier, Google, Stripe and Shopify have also purchased voluntary credits.

Carbon removal credits are often differentiated based on their durability, meaning how long the CO2 is expected to be stored. Permanent solutions come at a premium price point because there are fewer of them on the market and the demand for durable removals is high.

The removal market is creating demand signals for emerging technologies, supporting innovation and addressing historical emissions. Carbon removal projects tend to have higher costs with evolving methodologies as the technologies are still developing. Some compliance systems are beginning to recognize removal pathways, and so in the longer term we expect to see the markets converge.

Where Carbon Management Technologies Fit

Carbon management projects can often participate in multiple markets simultaneously, stacking credit generation to increase their economic benefit. However, caution is needed to avoid double counting the same reductions or removals across different markets. For example, a bioenergy project begins by growing crops. During growth, the crops absorb atmospheric CO2 through photosynthesis. Then the biomass (crops) is processed into ethanol. During the fermentation, concentrated CO2 is created and rather than venting that CO2, the facility can capture and inject it for permanent geological storage. At this point the atmospheric CO2 that was captured by the crop has been permanently stored, and this project could generate voluntary or carbon removal credits. In addition, the ethanol plant could be regulated under an output-based pricing system and may reduce its own compliance obligations or generate performance credits if it performs better than the benchmark. If eligible capture and storage activities could also generate offset credits. Then, ethanol could be blended with gasoline, reducing the carbon intensity of transportation fuels and generating CFR credits.

Canada’s carbon credit landscape is becoming increasingly sophisticated and overlapping. For project developers, understanding where projects fit, and where they may fit in the future, will be essential for maximizing value, attracting investment, and accelerating deployment.