In the crucial next couple of decades as governments and industry are moving toward net zero emissions, we have to use every tool available to us. Achieving consequential reductions in greenhouse gas emissions will take an all-of-the-above approach, including emerging technology pathways such as direct air capture (DAC).

What is DAC?

But first, what is DAC and how does it fit with other, more established carbon-reducing technologies such as carbon capture and storage (CCS)? The most developed DAC technologies remove carbon dioxide directly from the atmosphere, using either solid adsorbent methods or aqueous absorbent methods, creating diverted carbon that can either be injected into geological storage or used for secondary, non-emitting manufacturing processes.

In its current form, DAC is a relatively energy-intensive process. Of the two leading technologies, solid DAC (S-DAC) works at lower temperatures (80 to 1200C), and could be fuelled with low-emission energy such as renewables. Liquid DAC (L-DAC) requires higher-intensity heat (between 3000C and 8000C), so has been designed to use higher-emitting fuel sources such as natural gas, though these emissions would be captured within the process.

DAC is still in a nascent stage of development, and is inevitably more costly than conventional point source capture owing to the dilute nature of carbon in the atmosphere. The International Energy Agency (IEA) cost estimates for DAC currently land between $US125 and $US335 per tonne of CO2 captured in the case of a large-scale capture plant. However, the DAC industry is optimistic that this could be reduced to below $US100 as the technology is further developed.

Where does DAC fit into the net zero equation?

In its September 2022 report on DAC, the IEA stated that there are 18 direct air capture plants operating worldwide, capturing almost 0.01 MtCo2 per year. The largest existing plant, built in Iceland last year, captures 4,000 tonnes of CO2 per year. In the agency’s Net Zero by 2050 Scenario, DAC will be scaled up by 2030 to capture 60 MtCO2, as part of a forecast 1.6 Gt CO2 per annum for all CCUS solutions. Given current investment levels and intentions, the IEA deems this level of capture possible but only with a significant deployment and demonstration of lowered capture and energy costs.

Direct air capture innovator Carbon Engineering recently announced front-end planning and engineering for a proposed 1 MtCO2 plant in Texas that could refine the technology and be replicated to extract up to 30 MtCO2 on the same site. This is the second capture and storage plant that Carbon Engineering has underway in Texas’ Permian Basin, and is designed to build a commercial value proposition for the technology and engineering.

Advanced DAC projects have also been announced in locations including Chile, Norway, and the United Kingdom. Of the 11 facilities underway globally, the IEA estimates that together they will be capable of capturing approximately 5.5 MtCO2 per year by 2030, which is 700 times the current capture rate of all DAC facilities, but is still only 10 per cent of the capture needed to reach the agency’s full net zero scenario.

How does DAC get to the next level?

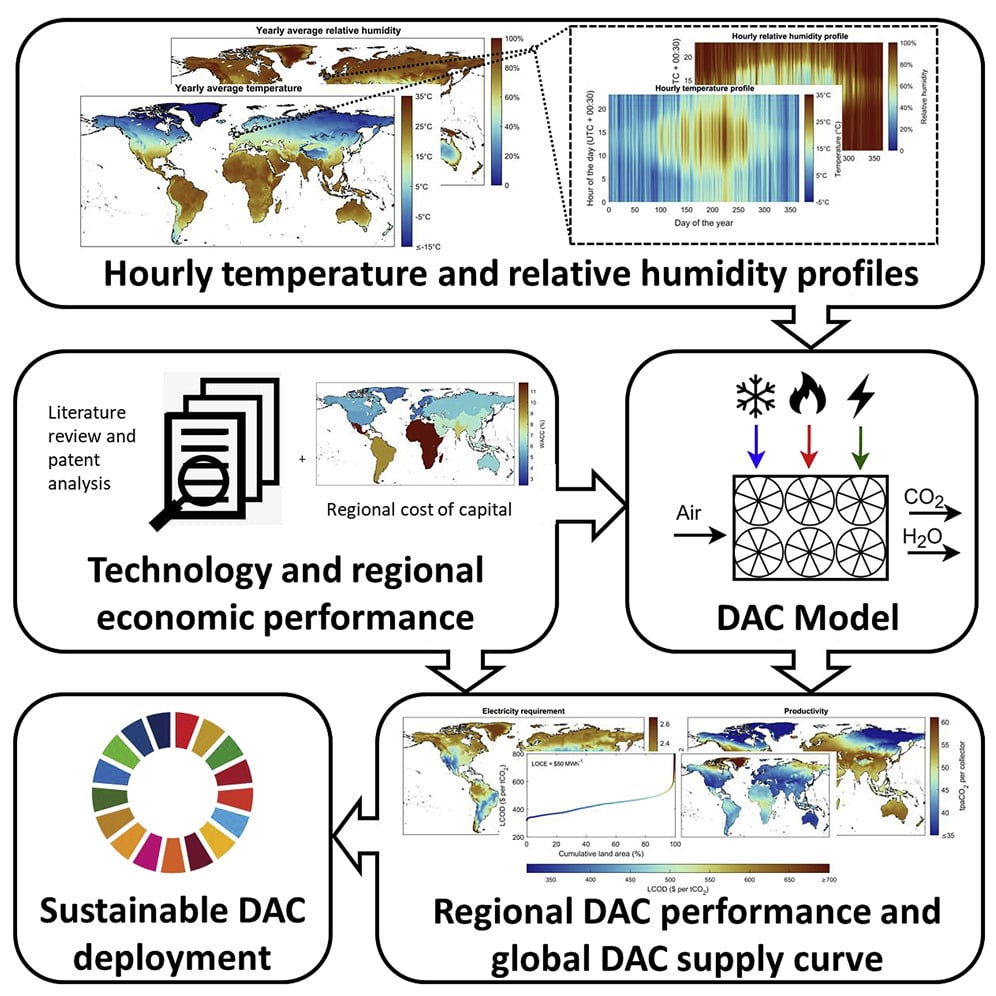

DAC technology performance is sensitive to changes in temperature and humidity, and given the significant investment needed to scale up operations to get closer to net zero targets, it is essential to identify regions around the world that will best accommodate DAC projects.

To determine this, colleagues and I at Imperial College London recently completed and published a detailed study into the long-term costs of DAC, with a particular focus on how costs may vary as a function of local conditions. The research led by Prof Paul Fennell shows that DAC is most effective in dryer, more moderate climates, and can be most readily accessed in northern geographical areas that have already established the investment value of emerging engineering for emissions reduction.

Our recently published study assessed the impact of regional climate variation on DAC performance, finding that approximately 25 per cent of the world’s land is unsuitable for deployment of DAC, and that colder, drier regions are most favourable. The study found that the cost of developing DAC capability is dependent on local climate, including both temperature and humidity, and on the local cost of energy.

Graphical Abstract of the paper “Geospatial analysis of regional climate impacts to accelerate cost-efficient direct air capture deployment” by Manwan Sendi, Mai Bui, Niall Mac Dowell and Paul Fennell published in One Earth, Volume 5 Issue 10 Pages 1153-1164 (October 2022):

One of the key next steps for scaling up DAC as an investment opportunity is to agree on a global life cycle assessment for captured carbon that will allow it to be included in regulated carbon markets. Efforts have begun in the United States and Europe to assess DAC-sequestered carbon for certification. The IEA cites several large companies, including Microsoft, Shopify, and Airbus who have already started to include DAC removal in voluntary carbon removal purchases, though DAC is not yet certified as meeting international mitigation targets under the United Nations Framework on Climate Change.

Meanwhile, DAC innovators are counting on exponential growth in the technology over the next decade. To meet ambitious climate targets, and to prove the technology is viable, investors and engineers will have to work quickly to make DAC a key factor in emissions reduction.

CarbonCapture expects its large-scale Project Bison DAC facility in Wyoming to be operational by the end of 2023 at a scale of 10,000 tonnes per year of carbon dioxide removed. The plan is to scale up to remove 5 MtCO2 per year by 2030, but will be built on a modular platform that could conceivably scale to what the company calls “no practical limits.” CarbonCapture is already listing the carbon credit assets of the project, with precisely metered accounting.

Government policy and private investment are just starting to coalesce around DAC, and the IEA describes it as gaining momentum. This year’s Inflation Reduction Act in the U.S. has already had an impact on the sector, providing substantially larger tax credits for carbon removal projects.

The United States government has also included DAC in its Carbon Negative Shot, launched at COP 26 last year in Glasgow – a portfolio of carbon direct removal approaches that have strong potential to reduce emissions at a scalable level and at a cost that will eventually approach less than $US100 / tCO2. With accurate certification, and a growing market for offsets, DAC could become even more cost-effective as an emerging technology. The next decade will set a foundation for the technology as a viable piece of the net zero puzzle.

Based in London, U.K., Niall Mac Dowell is Special Advisor to the International CCS Knowledge Centre. Niall represents the Knowledge Centre amongst global decision makers and financiers to accelerate the deployment of CCS. He is also a professor in Energy Systems Engineering at Imperial College London.